Did Federal Income Tax Change For 2018

The new tax law made substantial changes to the taxation rates and the revenue enhancement base of operations for the individual income revenue enhancement. The major provisions follow, excluding those that simply affect business organization income.

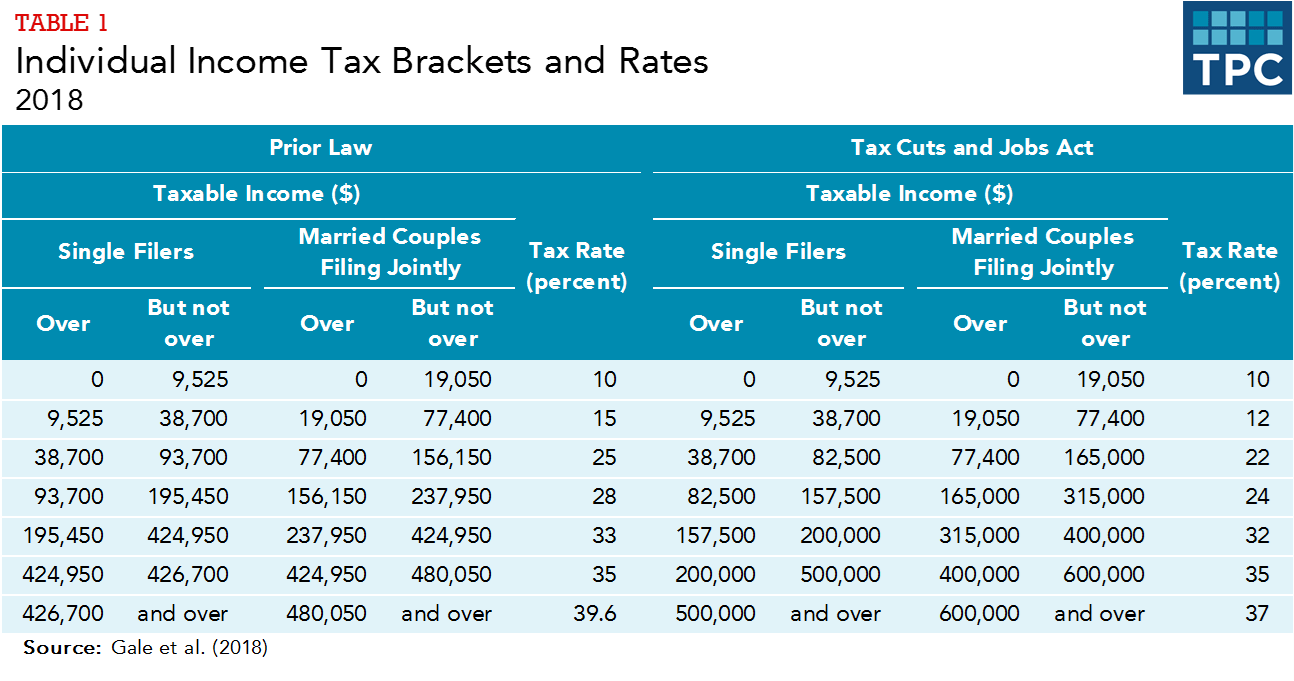

Tax Rates and Tax Brackets

The Tax Cuts and Jobs Human activity (TCJA) reduced statutory revenue enhancement rates at almost all levels of taxable income and shifted the thresholds for several income taxation brackets (table ane). As under prior law, the tax brackets are indexed for inflation but using a unlike inflation index (meet below).

Family Benefits (Personal Exemptions, Kid Credit)

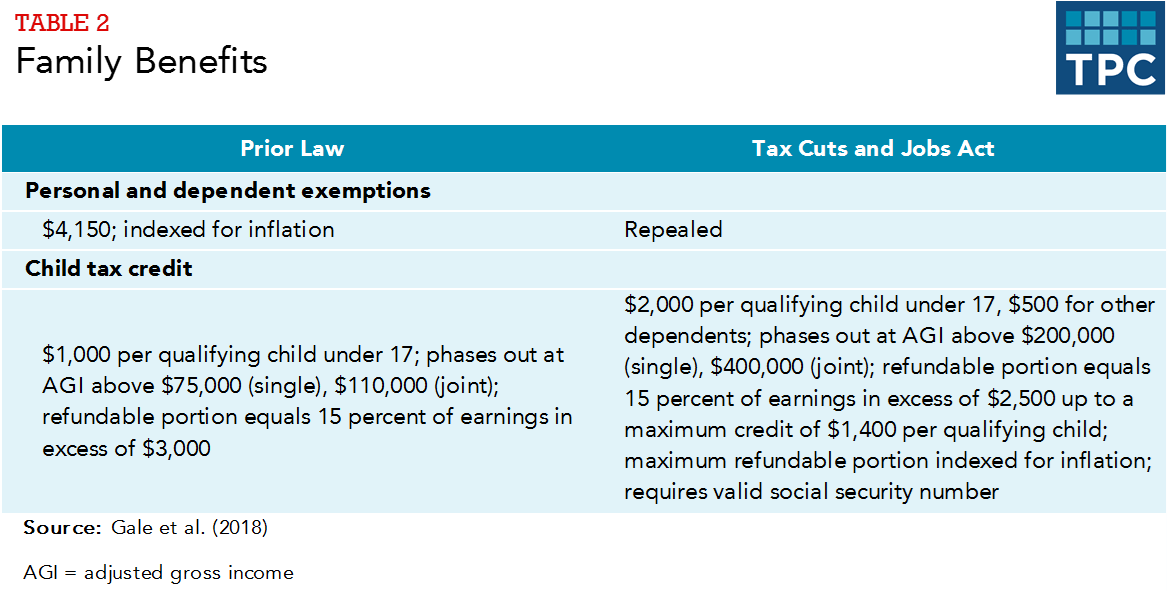

TCJA repealed personal and dependent exemptions. In place of personal exemptions, TCJA increased the standard deduction, discussed beneath. In place of dependent exemptions, TCJA increased the child taxation credit (CTC) and created a new $500 taxation credit for dependents not eligible for the child tax credit (table 2).

TCJA expanded the CTC in several ways. It doubled the maximum per kid credit amount from $one,000 to $two,000 starting in 2018. It too increased the refundable portion of the credit but limited the maximum refundable credit to $1,400 per child in 2018. The maximum refundable amount limit is indexed for inflation simply the maximum total credit amount is not. Unlike prior law, TCJA limited eligibility for the credit to children who have a valid social security number.

TCJA extended the CTC to college-income families by substantially increasing the income thresholds at which the credit phases out. As under prior police, the income phaseout thresholds are non indexed for inflation.

TCJA created a new nonrefundable $500 credit for other dependents, including children who are too old to exist eligible for the CTC, full-time college students, other adult members of the household for whom the taxpayer provides significant fiscal back up, and children who would otherwise exist eligible for the $2,000 child tax credit but lack a valid social security number. The $500 amount is also not indexed for inflation.

Standard And Itemized Deductions

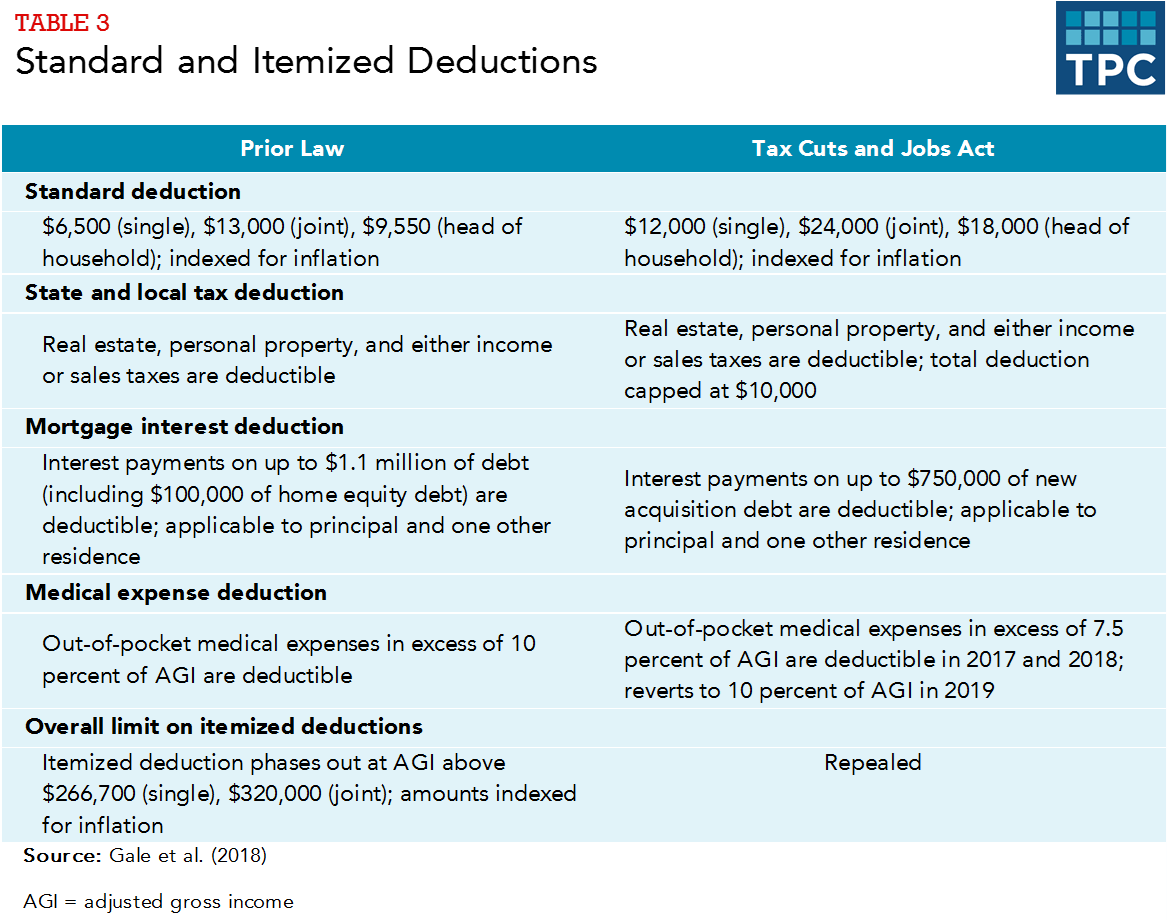

TCJA well-nigh doubled the standard deduction (table 3). Equally before, the standard deduction amounts are indexed for inflation. The larger standard deductions will essentially reduce the number of taxpayers choosing to catalog their deductions.

TCJA changed the structure of several major itemized deductions. Under prior law, itemizers could claim deductions for all state and local belongings taxes and the greater of income or sales taxes (subject to overall limits on itemized deductions). TCJA limited the itemized deduction for total land and local taxes to $x,000 annually, for both unmarried and articulation filers, and did non index that limit for inflation. As nether prior constabulary, taxpayers cannot claim a deduction for state and local taxes against the alternative minimum tax (AMT).

Under prior police force, taxpayers could deduct interest on mortgage payments associated with the starting time $one meg of principal paid on debt incurred to purchase (or essentially renovate) a primary and secondary residence plus the first $100,000 in home equity debt. For taxpayers taking new mortgages after the effective engagement, TCJA express the deductibility to the interest on the first $750,000 of loan principal and eliminated the deductibility of interest for home equity debt.

Previously, taxpayers could deduct out-of-pocket medical expenses (including costs for health insurance) above ten pct of adapted gross income (AGI). For 2017 and 2018, TCJA allowed deductions for out-of-pocket medical expenses to a higher place 7.5 percent of AGI. After 2018, the prior constabulary 10 per centum of AGI threshold applies.

TCJA repealed the phase-down of the amount of commanded itemized deductions (sometimes chosen the Pease provision). This limitation took upshot at AGI above $266,700 for single filers and $320,000 for taxpayers filing articulation returns.

majuscule gains, dividends, and the alternative minimum tax

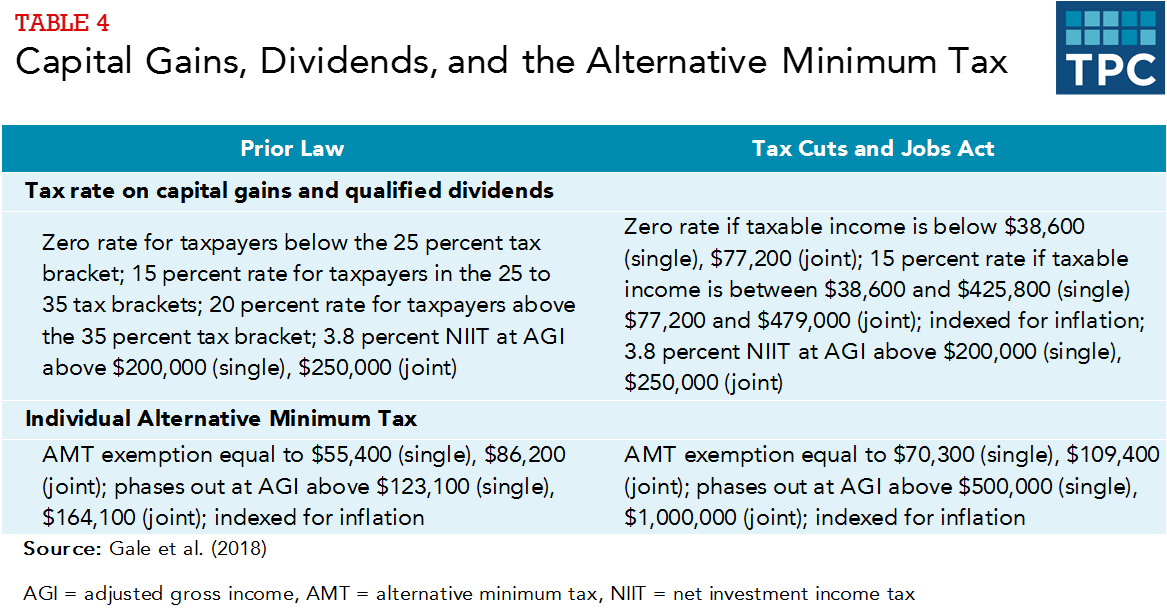

TCJA retained the preferential tax rates on long-term uppercase gains and qualified dividends and the three.8 percent net investment income tax (NIIT). The NIIT applies to involvement, dividends, short- and long-term majuscule gains, rents and royalties, and passive business organization income. TCJA separated the tax-charge per unit thresholds for capital gains and dividend income from the taxation brackets for ordinary income for taxpayers with college incomes (table iv).

TCJA retained the private AMT only raised the exemption levels and raised the income threshold at which the AMT exemption phases out, which will significantly reduce the number of taxpayers subject to the AMT. The exemption amounts and phaseout thresholds continue to be indexed for aggrandizement.

Estate Tax

TCJA doubled the estate revenue enhancement exemption to $11.ii 1000000 for single filers and to $22.4 million for couples, and continued to index the exemption levels for inflation (table 5). The top estate tax rate remains at 40 percent.

Affordable Care Act Penalty Tax

Starting in 2019, TCJA gear up the Affordable Care Act'due south (ACA'south) individual mandate penalty tax to zero. Previously, households without qualifying health insurance were required to pay a penalisation equal to the lesser of ii.five percent of household income or $695 per adult and $347.50 per child, upwards to a maximum of $2,085. Nether the new police, individuals who do non enroll in adequate health insurance plans will not face a penalty starting in 2019. Because fewer people volition obtain free or subsidized coverage in the absence of the penalty tax, and the reduced costs of ACA premium tax credits and other subsidies and Medicaid benefits will far exceed the lost acquirement from setting the penalization tax rate to zero, the internet effect will be to reduce the federal budget deficit. This provision does not dusk.

Inflation Indexing

TCJA changed the measure used for aggrandizement indexing, from the Consumer Toll Index for All Urban Consumers (CPI-U) to the chained CPI-U. The chained CPI-U more accurately measures changes in consumer welfare resulting from price changes considering information technology accounts for people finding substitutes for appurtenances whose prices increase faster than others. The chained CPI-U thus generally increases at a slower rate than the traditional CPI-U, implying that individuals volition end up in higher tax brackets and that indexed taxation credits (like the earned income tax credit) volition increment at slower rates than they would take under the old indexing organization. The change in indexing is permanent.

Sunsets

A notable feature of the individual tax and the estate revenue enhancement provisions is that all of them expire after 2025, except the reduction of the ACA penalty tax, the change in inflation indexing, and several changes in the taxation base of operations for business income. Some provisions elapse sooner (for example the increased deductibility of medical expenses applies only to tax years 2017 and 2018). In contrast, many of the business concern tax provisions do not sunset. Congress chose to make the individual provisions temporary to limit the acquirement toll of the TCJA to a level consequent with the overall constraint on the 10-year revenue loss in the Congressional Budget Resolution and to comply with Senate upkeep rules under the process used to pass the revenue enhancement deed that require no increase in the federal budget arrears afterwards the tenth yr.

Source: https://www.taxpolicycenter.org/briefing-book/how-did-tax-cuts-and-jobs-act-change-personal-taxes

Posted by: delgadogated1935.blogspot.com

0 Response to "Did Federal Income Tax Change For 2018"

Post a Comment